My family and I went on a hiking holiday recently, in Slovakia. It is my wife’s home country. We often go there, and the landscape is fantastic.

When we reached some of the smaller peaks in the Lower Tatras, I could not help thinking about how important the word ‘peak’ had become in my work recently.

I know you shouldn’t think of work while on holiday, especially when hiking, but alas, it happened.

In the first decade of the 21st century, the term ‘peak oil’ was in vogue. It was a way to suggest that the supply of oil is limited and that the world would soon reach peak production. Further production, the theory suggested, would hardly be able to keep up with demand. As a result, prices would explode, leading to a global crisis if the world did not diversify from oil as soon as possible.

There is no denying that diversification is good if you have viable, affordable alternatives that can be efficiently distributed. But the fundamental premise – that oil was running out – was flawed from the start.

I was part of the group of economists that argued that this peak of supply would not happen; there were simply too many oil resources onshore and offshore. Given significant investment and developing modern technology, there would be no shortage.

It took a while before this argument achieved traction. But eventually it got there. The shale revolution in the US, significant offshore developments and enhanced oil recovery in mature fields are now providing enough oil for decades to come.

The peak-oil story from a supply side of view vanished…

… just in time to make room for the peak oil story from the demand side: The new theory goes that in order to help to keep any increase in global temperature to well below 2 degrees Celsius, the world needs to reduce emissions sharply – including through the diminishing use of fossil fuels. These will peak soon and, as a result, companies investing in oil and gas exploration and production could be stuck with stranded assets.

Here is my take on that. First, I fully support the Paris Agreement. The world knows enough to act now. This means tackling the dual challenge: to provide more energy for a growing world population (with billions of people still lacking access to clean energy) while at the same time reducing emissions. And contrary to the peak oil story on the supply side, I fully agree that there will be a peak of oil demand some day in the future. Depending on the various 2c scenarios, this could happen within the next two decades.

As I see it, this discussion has three components. The first is the length of time it will take to reach peak demand. Second is the preparation being done by oil and gas companies to manage the transitions. The third part of this discussion involves the consequences for these companies – which could be smaller than anticipated.

Let’s look at each component in a bit of detail.

Global oil demand is still rising significantly. Today, the world needs about 100 million barrels of oil per day. That is about 2 litres per person per day. But of course, the distribution is unequal. For example, in the UK the figure is 4 litres per person. In the US it is about 9 litres. The Chinese consume 1.5 litres per day, while in India the figure is 0.5 litres. Obviously, there will be some catching up. Billions of people will move into the middle class within the next two decades, buying their first cars or making their first flights. (Even now, 80 per cent of mankind has never been in a plane!) This catching up, combined with a soaring oil demand for petrochemicals, is likely to increase oil demand for some time. But make no mistake, the demand will peak one day.

As for energy transitions: many IOGP members are integrated oil and gas companies. They not only produce crude oil, but they refine it and sell finished products like diesel, gasoline, kerosene, heating oil all over the world. And some have learned to operate in markets with falling demand. In my home country, Germany, demand for heating oil in 1975 was 45 million tonnes; now it is about 15 million tonnes. The number of service stations in 1970 was 45.000; now it is down to about 14.000. With that history, market changes or energy transitions are nothing new. So, I am confident that IOGP Members will not only be able to adapt but will be in the forefront of change.

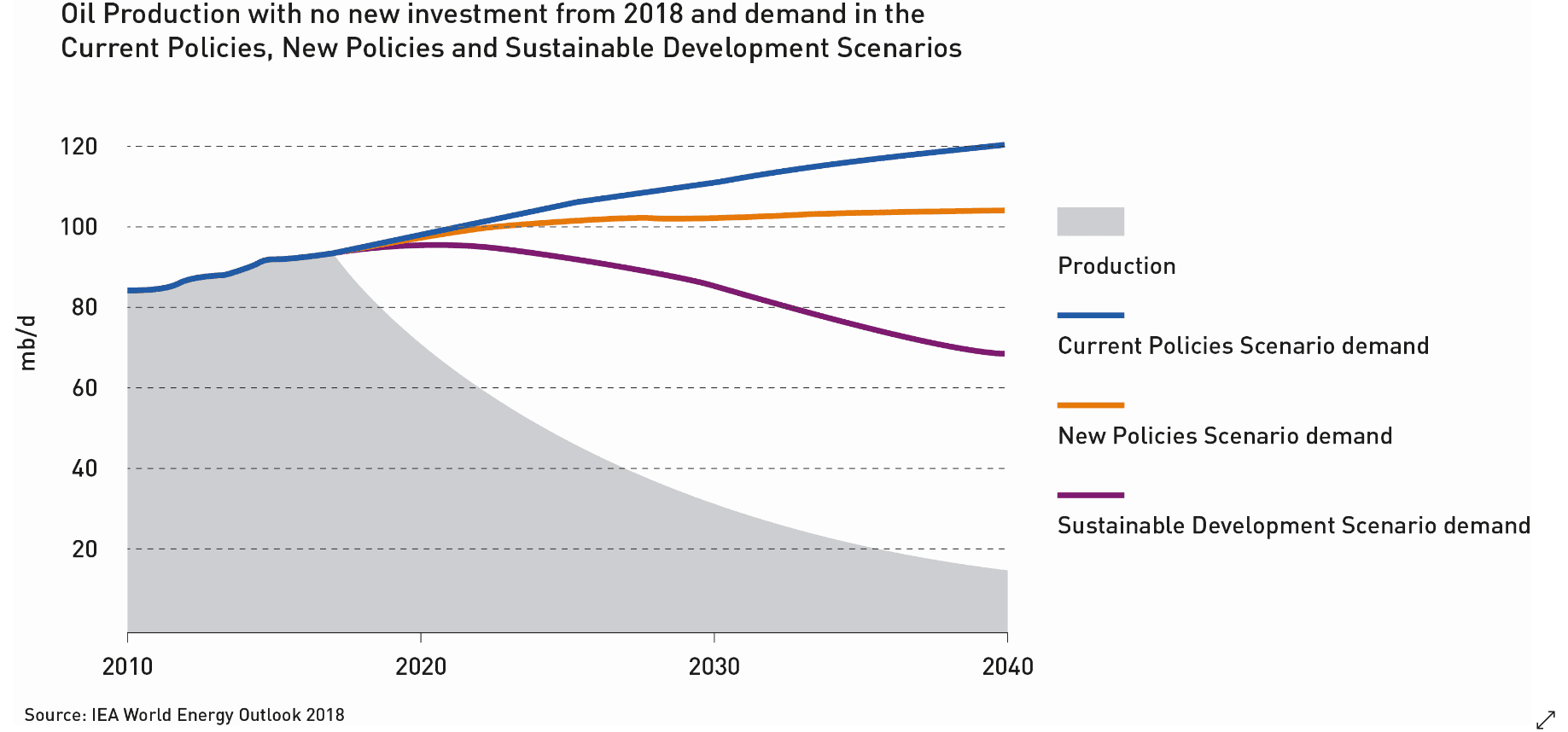

Thirdly, even when oil demand eventually does stop rising, oil companies will continue to invest just to make up for field depletion (see slide). As the International Energy Agency’s World Energy Outlook 2018 says, ‘The natural decline rate is the drop in production from all currently producing fields that would occur if capital investment were to cease immediately. If there were to be no further capital expenditure, total production globally would fall by over 8% per year till 2025…’. Thus, not investing in oil is not an option — not even when the demand goes down!

Thirdly, even when oil demand eventually does stop rising, oil companies will continue to invest just to make up for field depletion (see slide). As the International Energy Agency’s World Energy Outlook 2018 says, ‘The natural decline rate is the drop in production from all currently producing fields that would occur if capital investment were to cease immediately. If there were to be no further capital expenditure, total production globally would fall by over 8% per year till 2025…’. Thus, not investing in oil is not an option — not even when the demand goes down!

In Slovakia, we finally reached the peaks we were going for. In the oil industry, we are still sweating our way upwards. But descending can also be quite rewarding as I can confirm from our way back.

About Olaf Martins

Olaf is IOGP’s global engagement manager. He has over 25 years’ experience in the industry. Before joining IOGP Olaf was with ExxonMobil, where he held a number of senior public affairs roles, including most recently his position as ExxonMobil Central Europe Holding’s manager of government relations and media. Olaf’s educational background is in economics.